- Consumer spending saw little change, but rising prices will eventually force consumers to start saving up

- First Republic Bank’s failure has only exacerbated even tighter lending standards which may persist to 2024

- Print shop owners need to be acutely aware of unexpected headwinds that may occur in the months ahead

Trends have remained relatively unchanged since our last report, but there are growing concerns over a possible financial crisis with the failure of First Republic Bank and PacWest Bancorp’s shaky position. With another case of economic uncertainty still looming threateningly over everyone’s heads, what can we expect in the coming weeks?

Consumer Spending Still on Trend

Let’s start with what we know first.

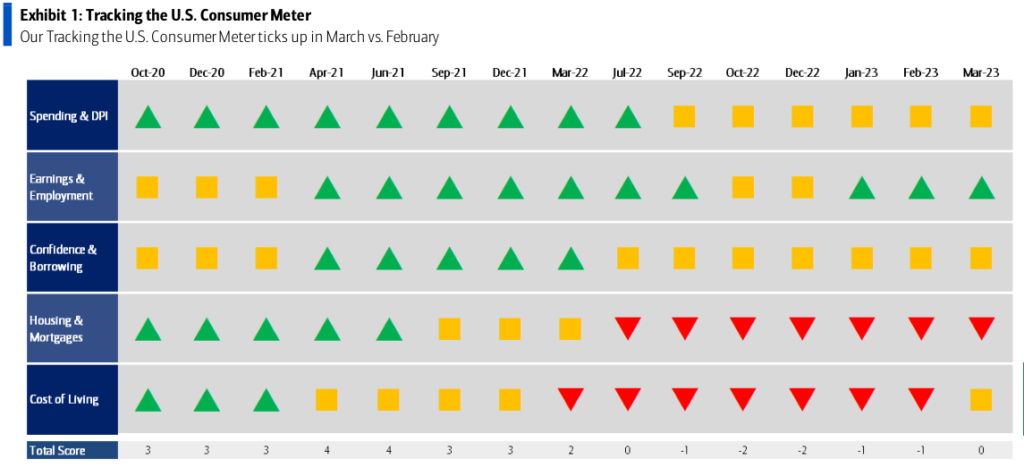

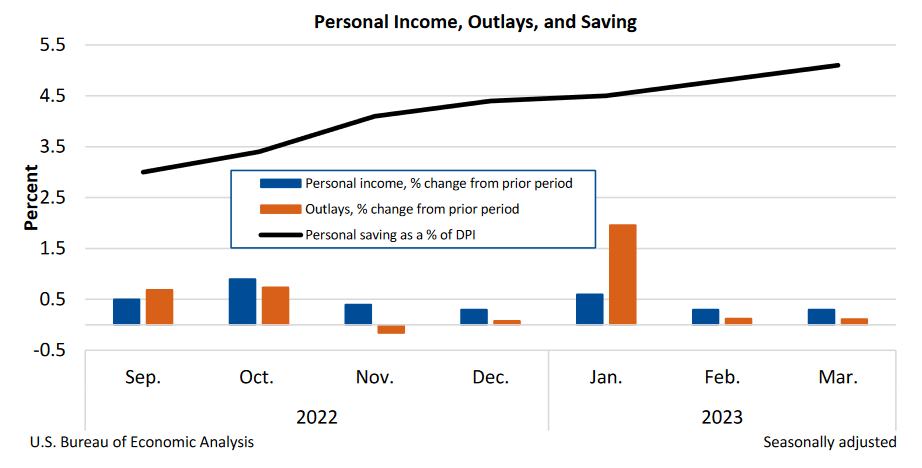

The good news is that consumer spending is still relatively good. In fact, real consumer spending went up to a decent 3.7 percent quarter-over-quarter, going up from the previously recorded 1.0 percent. Personal savings also grew to 5.1 percent in March (April figures have not been released as of yet), up from 4.8 percent in February 2023.

It’s both strong nominal and real income levels that are keeping consumer spending going. Just look at the luxury goods segment: LVMH, the parent company of luxury brands like Louis Vuitton, became the first European company to exceed $500 billion in market value, with a “17 percent rise in first-quarter sales” in early April. Meanwhile, designer brand Hermes posted a profit of $3.6 billion in 2022 despite the economic uncertainties that year; this was a 38 percent increase from 2021.

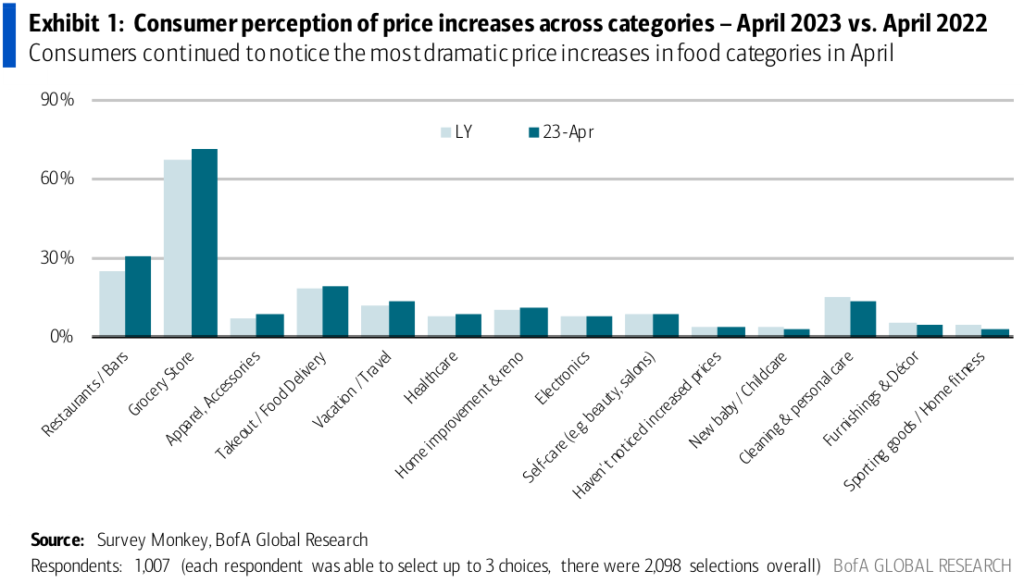

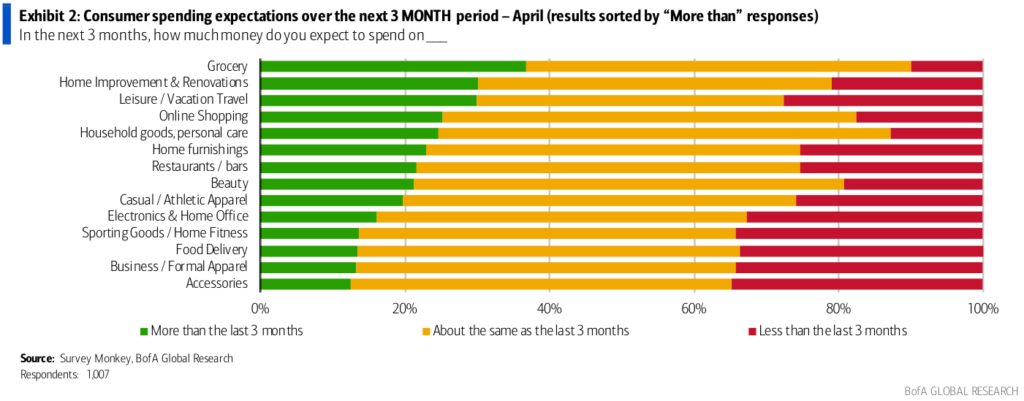

However, consumer spending will likely be a mixed bag for the rest of the year. Many consumers expect to spend more on groceries, home improvement, utilities, and travel. Both home improvement and vacationing/travel saw the largest year-on-year percentage change in April 2023 for “expectations for the most dramatic increase in spending over the next 12 months.”

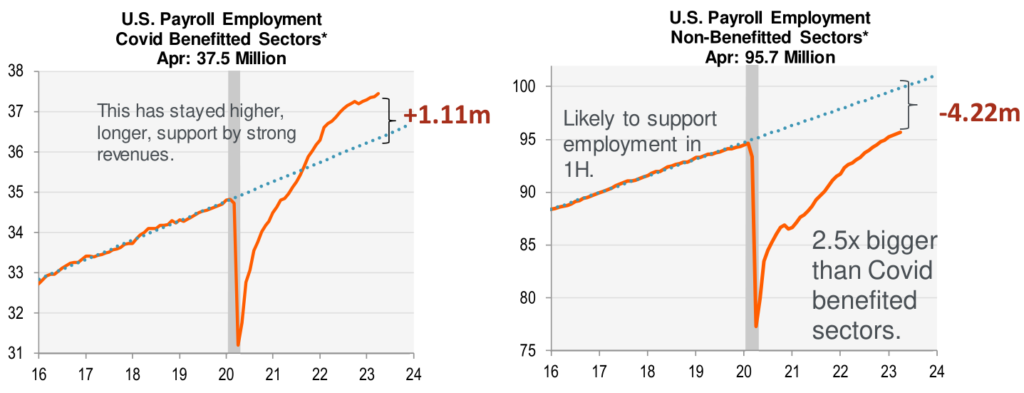

Foot traffic, in particular, has seen Covid-benefitted sectors weaker in April: foot traffic for home improvement fell way below pre-Covid trends, while department stores, fitness, hotels, and casinos have also seen a slight drop. Dining, leisure & recreation, and discount stores continue to do well despite fluctuations.

Consumers are still careful about where they spend their money. They’re also becoming more aware of how prices have increased since last year. Lower-income groups, in particular, are more likely to have higher 3-month spending expectations in online shopping and groceries than higher-income groups, prioritizing only what’s necessary and looking out for deals on everyday items.

Trends remain strong in home improvement and travel, especially among the upper-income segment of Americans. It would be wise to abide by our previous suggestion to market custom products in popular niches. Partner with airlines and travel companies (if you haven’t already) in your area and grow your online presence if you haven’t already done so. Alternatively, look at popular travel niches (e.g., gift shops) and seek out opportunities in those areas.

Home improvement and home decor may not be doing as well, but the aforementioned consumer surveys suggest that consumer expectations for these segments may increase in the coming months. It’s a good idea to partner with home improvement companies in the near future.

Be on the lookout for rising credit card delinquency rates! Despite the seemingly higher wages and steady consumer spending, delinquencies for payments that are 90 days late (or higher) went up to 5.32 percent, up from 5.16 percent in the previous quarter. Younger Americans between 18 to 29 years of age continue to have the highest delinquency rates at 9.36 percent. It may be best to have clear payment terms, such as requiring a minimum deposit on orders, before you take on any potential orders.

The question is, if consumer spending is still going strong, why do experts say that a recession is still on the cards?

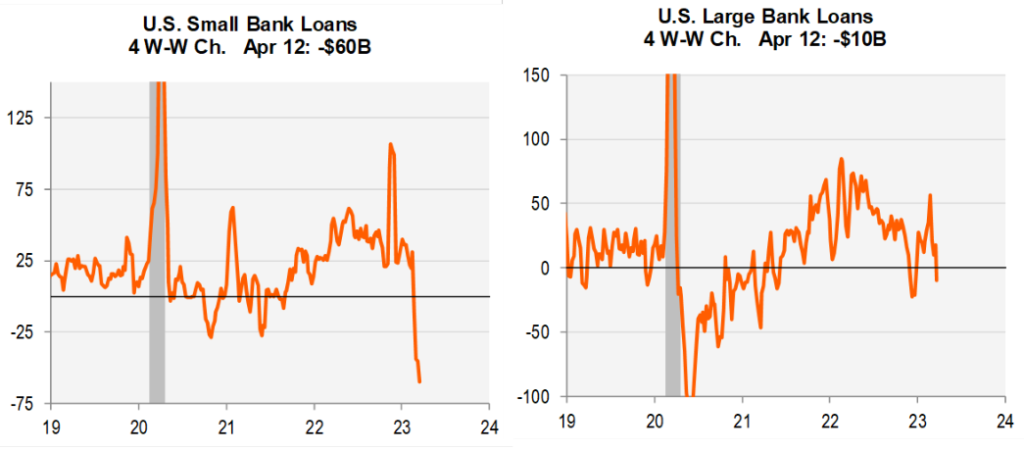

Lending Standards Still Tight

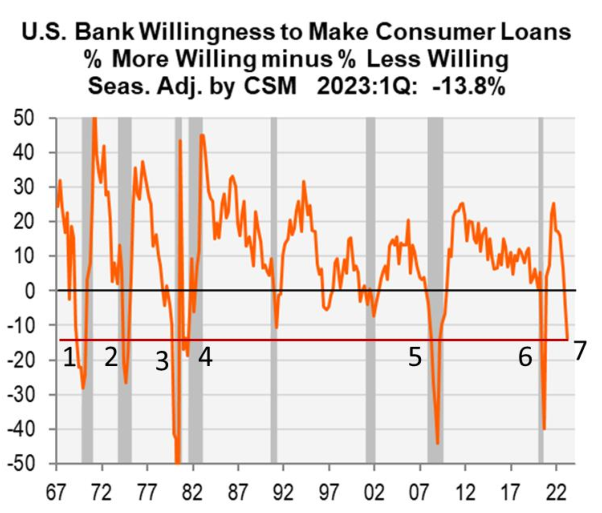

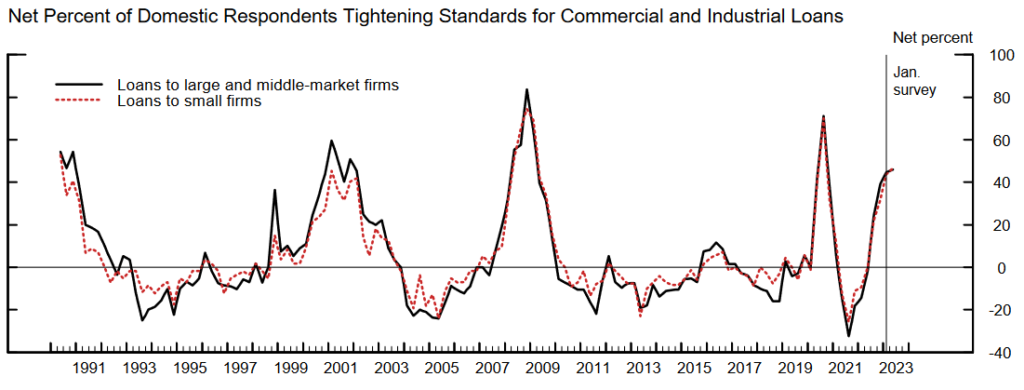

With the sudden shock of First Republic’s failure and PacWest Bancorp’s shaky situation (which has since seen a recent rebound that started last Friday), worries about an impending wave of further bank collapses have surged once more. In the meantime, banking lending standards have been inflationary for a substantial amount of time, well before Silvergate and Silicon Valley Bank’s failures. From here on, it’s going to get tighter still.

In fact, the Federal Reserve’s latest Senior Loan Officer Survey (SLOS) indicates “weaker demand” for commercial and industrial loans, which may be exacerbated further by the Fed’s decision to hike interest rates by a quarter percentage point. The SLOS also indicates that these woes will undoubtedly persist into the following year.

These tight lending standards might become the main cause of the recession. In general, tight lending means less money available to both consumers and companies, which in turn reduces overall spending. Every time lending standards have been this tight, a recession isn’t far off. Given that the Fed could potentially raise interest rates yet again in June, in its bid to combat inflation, this could spell trouble for the economy.

As it is, lending is already starting to shrink, and it’s not going to improve any time soon.

It would be wise to bolster your finances now and refrain from taking on new loans for your shop’s expansion or procuring new equipment. If you’re still adamant about upgrading your shop, make sure you plan ahead and take stock of your shop’s current financial position. Weigh your financing options carefully, as high interest rates and steep repayment schemes can take a hefty bite out of your cash flow.

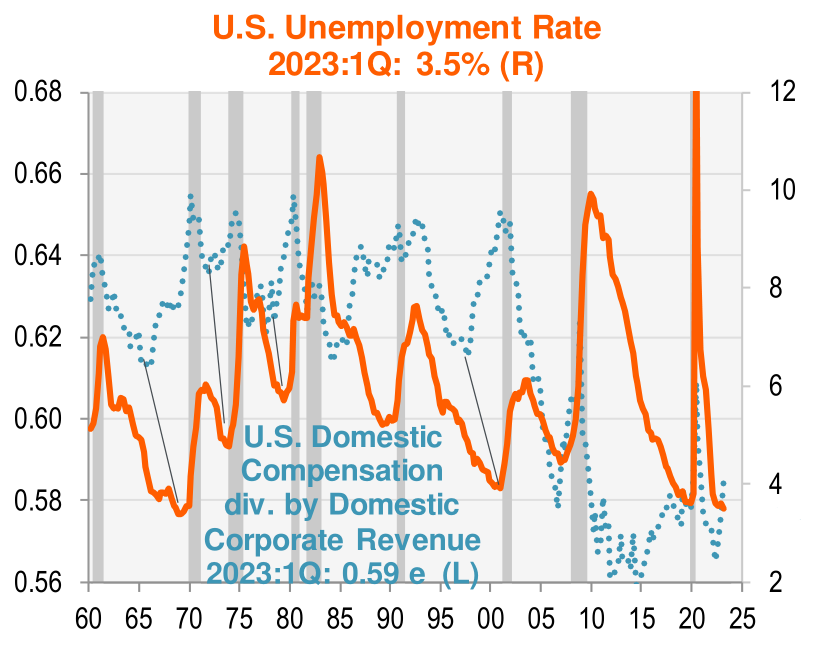

Unemployment Figures Fluctuating

Now here’s where things get a little blurry.

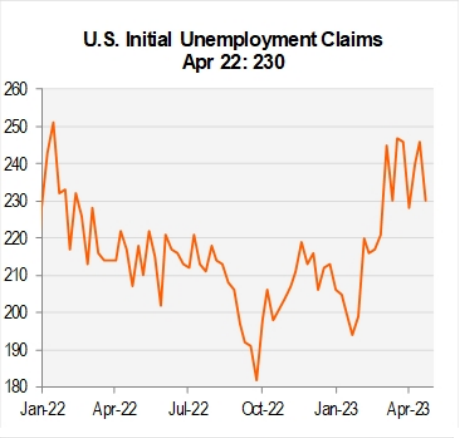

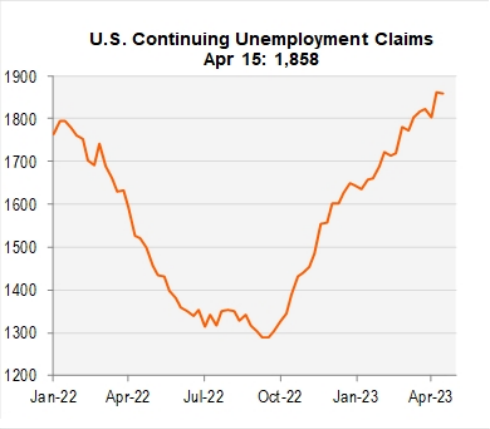

Since the previous revision to reporting standards, unemployment claims have seen significant fluctuations. Initial unemployment claims had initially increased by 5,000 week-over-week to 245,000, up from the estimated 240,000 claims, before going down 16,000 to 230,000 as of April 27th.

Continuing claims are still on an uptrend, increasing by 61,000 to 1.865 million – a rather shocking number – before ticking down by 3,000 to 1.858 million the week after (as of April 27th). As of last week, this number has since fallen to 1.805 million.

The unemployment rate has not strayed far from previous values, with the rate in April at 3.4 percent – down from 3.5 percent in the previous month. There are currently 1.6 job openings for every unemployed person in March, which many economists still view as inflationary. Even as Covid-benefitted sectors are still laying off employees, non-benefited sectors – including hotels and food service – are still looking to refill vacancies.

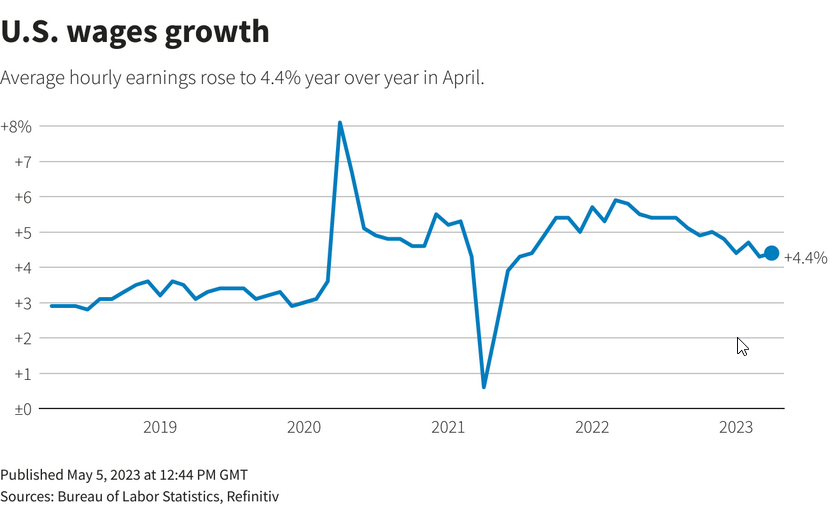

Currently, average hourly earnings went up 0.5 percent in April after a hike of 0.3 percent back in March. This reflects a 4.4 percent year-on-year increase in private nonfarm payrolls in April (compared to 4.3 percent in March). You can see how, despite some alarming changes in total claims, the overall job outlook is rather confusing since the labor market is still looking strong.

Fewer workers are also quitting their jobs, highlighted by how quits are now well below the highs of December 2021. However, this is bound to change once companies start cutting their losses by laying off staff, and unemployment soon follows. Expectations that the recession will start in Q4 or later remain strong.

If you’re still looking to hire new staff, you should do so quickly. Take note of the number of positions you need to be filled, and ensure you won’t be overhiring.

Inflation is Still Slowing (At a Snail’s Pace)

The annual inflation rate has slowed down yet again to 4.9 percent in April 2023, below its 5 percent forecast. The consumer price index (CPI) only increased 0.4 percent last month, notably impacted by higher prices for gas, housing, and used cars. This is a sign that the Fed’s moves to curb inflation are working, though still at a very slow pace.

While the GDP deflator – which measures the “changes in prices for all the goods and services” made in a country – saw a slight uptick due to high consumer prices and capital expenditures (or capex), inflation looks set to remain on a downturn. This is what everyone is hoping will happen next, despite the current stickiness.

Strong nominal GDP growth, fueled by the high liquidity the Fed still needs to tangle with, will also “support corporate revenues near-term.” Note that much of the increase in spending is attributed to companies raising prices, thus impacting affordability. As prices soar and personal savings diminish, corporate profits will reverse to recoup mounting losses.

The labor market needs to weaken for the Fed to achieve its 2 percent inflation target. Strong unit labor costs (ULCs) keep prices and incomes high; as prices soar and personal savings diminish, corporate profits will reverse to recoup mounting losses. As a result, compensation ratios (how much companies need to pay its employees) will rise, leading to unemployment peaking at 5.5 percent later this year.

Stay Prepared As Always

Our cautious optimism has remained since our previous article. However, we’d still advise caution, given how consumer spending can still turn on a dime at any given moment. These are rather confusing times with prices still high, unemployment at record lows, and yet people are still struggling to make ends meet.

Moreover, while the Fed may be mulling over a pause to further interest rate hikes, it’s still too early to say if they’ll actually refrain from it.

“Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain.”

Federal Reserve press release, dated May 3, 2023

The government will no doubt find ways to delay the recession as best as possible. Government spending increased in the first quarter of this year, indicating that “fiscal policy may be more expansionary” to facilitate this, especially with elections looming on the horizon.

You should keep your shop busy for now and seek out opportunities wherever you can, such as county events or even state elections. As long as you take stock of your finances, you’ll be able to weather the effects of a recession better when it finally comes.